-

Coastal Financial Corporation Announces Fourth Quarter and Year End 2020 Results

ソース: Nasdaq GlobeNewswire / 27 1 2021 08:27:01 America/Chicago

2020 Highlights:

- Net income totaled $15.1 million for the year ended December 31, 2020, or $1.24 per diluted common share, an increase of 14.0% from $13.2 million, or $1.08 per diluted common share, for the year ended December 31, 2019.

- Basic earnings per share increased 30.0%, and diluted earnings per share increased 26.7%, for the quarter ended December 31, 2020, compared to the quarter ended December 31, 2019.

- An $8.3 million provision for loan losses was recorded during the year ended December 31, 2020, largely due to continued economic uncertainties from the COVID-19 pandemic.

- Total assets grew $637.6 million, or 56.5%, to $1.77 billion for the year ended December 31, 2020, compared to $1.13 billion at December 31, 2019.

- Total loans receivable, net, including $365.8 million in PPP loans, grew $608.0 million, or 64.7%, to $1.55 billion for the year ended December 31, 2020, compared to $939.1 million at December 31, 2019.

- Total deposits increased $453.3 million, or 46.8%, to $1.42 billion for the year ended December 31, 2020, compared to $968.0 million at December 31, 2019.

EVERETT, Wash., Jan. 27, 2021 (GLOBE NEWSWIRE) -- Coastal Financial Corporation (Nasdaq: CCB) (the “Company”), the holding company for Coastal Community Bank (the “Bank”), today reported unaudited financial results for the quarter and year ended December 31, 2020. Net income for the fourth quarter of 2020 was $4.7 million, or $0.38 per diluted common share, compared with net income of $4.1 million, or $0.34 per diluted common share, for the third quarter of 2020, and $3.6 million, or $0.30 per diluted common share, for the quarter ended December 31, 2019.

“If there is one thing 2020 has taught us, it’s how resilient we are. Those words ring true time and time again as we continue to navigate our way through these unprecedented times. Despite the disruptions and economic uncertainty resulting from the COVID-19 pandemic, we are pleased to announce that we finished the year with $15.1 million in net income, which includes $8.3 million in provision for loan losses, primarily in response to the economic uncertainties of the COVID-19 pandemic. To date we have not seen a significant shift in our credit quality metrics, yet there are still economic uncertainties that exist. Deposit growth was strong, increasing $453.3 million, or 46.8%, in 2020, with core deposits totaling $1.3 billion, or 93.4% of total deposits, at December 31, 2020.

“As a preferred Small Business Administration (“SBA”) lender, we are committed to working with the SBA to provide financial assistance to existing and new small business customers via the third round of PPP loans as provided in the Coronavirus Aid, Relief and Economic Security Act (“CARES Act”), which opened for applications on January 19, 2021. I am proud to report that as of January 25, 2021, we have accepted applications for $233.6 million, representing 1,385 new and existing customers, in this latest round of PPP loans, consisting of $14.7 million in new PPP applications for first draws and $218.9 million in a second draw for small businesses that previously received PPP funds. Our growing CCBX division continues to develop and provide an additional source of fee income for the Company. CCBX provides Banking as a Service (“BaaS”) enabling broker dealers and digital financial service providers to offer their clients banking services. We are hard at work on CCDB, our digital banking division, and look forward to introducing our digital bank accounts later this year in connection with our previously announced collaboration with Google Pay. We recently went live with our new mobile wallet product which provides our customers with more ways to pay,” stated Eric Sprink, the President and CEO of the Company and the Bank.

“The health and safety of our employees and customers is of utmost importance, and as such we continue to enhance and modify measures already in place to keep us all healthy and safe while remaining open and serving our customers at our drive-throughs, by appointment, call center, mobile banking, online banking and ATMs. In addition, the Company continues to successfully employ remote work arrangements to the fullest extent possible. We remain committed to our customers, communities and employees as we move into this new year. The road ahead may be uncertain, but we are dedicated to strengthening existing relationships and embracing new opportunities for growth by continuing to focus on our three prong strategy of growing our core community bank, growing CCBX, our BaaS division, and building CCDB, our digital banking division.”

Results of Operations

Net interest income was $16.9 million for the quarter ended December 31, 2020, an increase of 12.2% from $15.1 million for the quarter ended September 30, 2020, and an increase of 49.4% from $11.3 million for the quarter ended December 31, 2019. The increase compared to the prior quarter and prior year’s fourth quarter is largely related to increased interest income resulting from loan growth. This loan growth included $365.8 million in PPP loans as of December 31, 2020, which contributed $2.8 million in net deferred PPP fees recognized, which is an increase of $347,000, or 14.2%, when compared to the quarter ended September 30, 2020, and $1.0 million in interest from the 1.0% contractual interest rate, for a total of $3.8 million in interest income for the quarter ended December 31, 2020.

As of December 31, 2020, $7.1 million, or 55.2%, of the total $12.9 million in PPP net deferred fees on PPP loans have been fully earned, with $5.8 million remaining to be recognized in interest income along with interest on loans. Net deferred fees on PPP loans are earned over the life of the loan, as a yield adjustment in interest income. Forgiveness of principal, early paydowns and payoffs on PPP loans will increase interest income earned in those periods from the recognition of PPP deferred fees.

Also contributing to the increase in interest income is fee income recognized on loans made through the Main Street Lending Program (“MSLP”). During the quarter ended December 31, 2020, we recognized $383,000 in earned fees through MSLP loans, and there was no fee income on MSLP loans in previous quarters.

Our yield on loans receivable was 4.64% for the three months ended December 31, 2020, compared to 4.33% for the three months ended September 30, 2020, and 5.36% for the three months ended December 31, 2019. In the first three quarters of 2020 we generally saw a decrease in loan yield resulting from the lower interest rate that PPP loans earn and downward repricing of our variable rate loans in the low interest rate environment. The increase in yield on loans receivable for the quarter ended December 31, 2020 was due to the addition of higher rate, non-PPP loans that were added during the quarter along with the recognition of deferred fees on PPP loans that were forgiven and paid off during the quarter ended December 31, 2020, as well as fee income recognized on MSLP loans. MSLP loans were established by the Federal Reserve to support lending to small- and medium-sized businesses that were in sound financial condition prior to the COVID-19 pandemic. The Federal Reserve purchases participations on these loans, with the Bank retaining approximately 5% of the outstanding balance. Management concluded that the sold portion of the MSLP loans qualified for sale accounting. The MSLP loans have a five year maturity with deferral of principal payments for two years and deferral of interest payments for one year. The program stopped purchasing participations on January 8, 2021.

Non-PPP loan growth was $122.0 million, or 11.5%, for the quarter ended December 31, 2020, compared to the quarter ended September 30, 2020, and this included CCBX loan growth of $21.8 million for the quarter ended December 31, 2020. The average rate on new loans was approximately 4.26%, compared to an average rate of approximately 3.44% for the quarter ended September 30, 2020. Interest and fees on loans was $1.6 million higher compared to the three months ended September 30, 2020 and $5.6 million higher than the three months ended December 31, 2019 due to increased loan balances, increased average interest rate, recognition of PPP deferred fees on PPP loans that were forgiven and paid off and recognition of fee income on MSLP loans. Interest income from interest earning deposits with other banks decreased $23,000, and $401,000 from September 30, 2020 and December 31, 2019, respectively, to $76,000 for the three months ended December 31, 2020, compared to $99,000 and $477,000 the three months ended September 30, 2020 and December 31, 2019, respectively, as a result of lower interest rates.

Interest expense was $1.2 million for the quarter ended December 31, 2020, a $133,000 decrease from the quarter ended September 30, 2020 and a $538,000 decrease from the quarter ended December 31, 2019. The interest expense decrease occurred despite an increase in average interest bearing deposits for the quarter ended December 31, 2020 of $29.2 million and $59.8 million, over the quarter ended September 30, 2020 and December 31, 2019, respectively, as a result of lower interest rates. Interest expense on borrowed funds was $407,000 for the quarter ended December 31, 2020, compared to $418,000 and $192,000 for the quarters ended September 30, 2020 and December 31, 2019, respectively. This increase from the quarter ended December 31, 2019 was primarily the result of the PPPLF borrowings, which were obtained to provide liquidity to fund the PPP loans; the decrease from the quarter ended September 30, 2020 is the result of a decrease in average PPPLF borrowings due to paydowns on PPP loans.

Net interest income increased $15.4 million, or 36.6%, to $57.4 million for the year ended December 31, 2020, compared to $42.0 million for the year ended December 31, 2019. These increases are largely related to increased interest income resulting from loan growth, the recognition of deferred fees on PPP loans that have been forgiven and paid off, and the additional fee income recognized on MSLP loans. Interest and fees on loans increased $16.6 million, or 36.5%, over the prior year period, despite a decrease in yield on loans receivable of 0.74% for the year ended December 31, 2020, compared to the year ended December 31, 2019. Non-PPP loan growth of $248.0 million, which includes CCBX loan growth of $65.3 million, for the year ended December 31, 2020, compared to the year ended December 31, 2019, contributed to this increase. Also contributing to the increase in loans is $365.8 million in PPP loans as of December 31, 2020. An average balance of $302.7 million in PPP loans contributed $3.0 million from the 1% interest rate and $7.2 million in fees recognized, for a total of $10.2 million in interest income on PPP loans for the year ended December 31, 2020, compared to the year ended December 31, 2019. Interest and fee income on MSLP loans also contributed to the increase, and was $398,000 for the year ended December 31, 2020, compared to no income on MSLP loans for the year ended December 31, 2019. Net deferred fees on PPP loans are earned over the life of the loan, as a yield adjustment in interest income. Forgiveness of principal, early paydowns and payoffs on PPP loans will increase interest income earned in those periods from the recognition of PPP net deferred fees. Interest income from interest earning deposits with other banks decreased $1.8 million, or 72.6%, to $663,000 for the year ended December 31, 2020, compared to $2.4 million for the year ended December 31, 2019, as a result of lower interest rates. Interest expense decreased $924,000, or 14.1%, to $5.7 million for the year ended December 31, 2020 compared to $6.6 million for the year ended December 31, 2019. Lower interest rates resulted in a decrease in interest expense despite a $158.6 million increase in average interest bearing deposits and $144.0 million increase in average borrowings for the year ended December 31, 2020, compared to the prior year period. Borrowings included $124.1 million in average PPPLF borrowings, which were obtained to partially fund the PPP loans.

Net interest margin widened in the quarter ending December 31, 2020 and will likely fluctuate over the near term as round one and round two PPP loans are forgiven and round three PPP loans are on-boarded. Accelerated deferred fee recognition related to the forgiven PPP loans supplemented interest income resulting in a net interest margin for the quarter ended December 31, 2020 of 3.89%, a 28 basis point increase from 3.62% for the quarter ended September 30, 2020 and a 37 basis point decrease from 4.26% for the quarter ended December 31, 2019. The increase over the prior quarter is due to the increase of higher rate, non-PPP loans coupled with the recognition of PPP deferred fees on PPP loans that paid down or paid off during the quarter ended December 31, 2020. The decrease in net interest margin from the quarter ended December 31, 2019 was largely a result of the low interest rate on PPP loans and lower interest rates on all other loans, especially our variable rate loans. PPP loans accounted for an average of $424.3 million in gross loans for the quarter ended December 31, 2020, and bear a contractual interest rate of 1.0%, and yield approximately 3.61% after considering the amortization of deferred PPP loan fees, for the quarter ended December 31, 2020. Cost of funds decreased four basis points in the quarter ended December 31, 2020 to 0.29%, compared to the quarter ended September 30, 2020 and decreased 41 basis points from the quarter ended December 31, 2019. Deposits into noninterest bearing and low interest bearing accounts by new and existing customers contributed to the reduced cost of funds. In addition, the Federal Open Market Committee (“FOMC”) lowered the Fed Funds rates five times for a total decrease of 2.25% since June 2019, which has impacted market rates paid on deposits. The lower interest rate environment will continue to impact the Company's net interest margin. Net interest margin for the year ended December 31, 2020 decreased 40 basis points compared to the year ended December 31, 2019 as a result of the low rate on PPP loans and lower rates on all other loans, especially our variable rate loans. Cost of funds decreased 33 basis points to 0.40% for the year ended December 31, 2020 compared to 0.73% for the year ended December 31, 2019. Growth in new and existing noninterest bearing deposit accounts and the lowered Fed Funds rates contributed to the reduced cost of funds.

During the quarter ended December 31, 2020, the average balance of total loans receivable increased by $40.5 million, to $1.53 billion, compared to $1.49 billion for the quarter ended September 30, 2020, as a result of loan growth. New loans in the fourth quarter of 2020 had an average interest rate of approximately 4.26%, compared to approximately 3.44% for the quarter ended September 30, 2020. Non-PPP loans grew by $122.0 million, or 11.5%, during the quarter ended December 31, 2020. PPP loans totaled $365.8 million as of December 31, 2020, which is a decrease of $87.0 million compared to the quarter ended September 31, 2020. PPP loans bear a contractual interest rate of 1.0%, yielding approximately 3.61%, after considering the amortization of deferred PPP loan fees. The average balance of total loans receivable at December 31, 2020 increased by $622.2 million to $1.53 billion, compared to $911.4 million for the fourth quarter of 2019, due to overall growth in the loan portfolio, combined with the aforementioned growth in PPP loans. Non-PPP loans grew by $248.0 million, or 26.4%, to $1.19 billion for the year ended December 31, 2020. Total yield on loans receivable for the quarter ended December 31, 2020 was 4.64%, compared to 4.33% for the quarter ended September 30, 2020, and 5.36% for the quarter ended December 31, 2019. The increase in yield on loans receivable over the quarter ended September 30, 2020 was a result of new higher rate, non-PPP loans added during the fourth quarter, combined with the recognition of PPP deferred fee income on PPP loans that paid down or paid off as well as fee income recognized on MSLP loans. The reduction in yield on loans receivable compared to the quarter ended December 31, 2019 was a result of the lower rate that PPP loans bear and the downward repricing of our variable rate loans in the low rate environment. PPP loans reduced the yield on loans receivable* by 36 basis points for the quarter ended December 31, 2020.

Contractual yield on loans receivable, excluding earned fees approximated 3.66% for the quarter ended December 31, 2020, compared to 3.61% for the quarter ended September 30, 2020, and 5.15% for the quarter ended December 31, 2019. During the quarter ended December 31, 2020, the average balance of PPP loans was $424.3 million. These loans bear a contractual rate of 1.0%, which negatively impacted the average contractual yield on loans. Excluding PPP loans and their related earned fees and interest, the contractual yield on loans receivable approximated 4.65%*. Also contributing to the reduction in contractual yield was the reduction in rates by the FOMC, which has resulted in lower rates on our variable rate loans and on new and renewing loans. Although we have rate floors in place for $398.6 million, or 25.6%, in existing loans, the rate reductions by FOMC has a corresponding impact on yield on loans receivables and the net interest margin in future periods.

Cost of deposits for the quarter ended December 31, 2020 was 0.22%, a decrease of five basis points from 0.27% for the quarter ended September 30, 2020, and a 41 basis point decrease from the quarter ended December 31, 2019. Deposit growth in new and existing noninterest bearing and low interest bearing accounts contributed to the reduced cost of funds in conjunction with rate reductions on deposits. We gained new customer relationships by making PPP loans to noncustomers that continue to move their deposit relationships to the Bank. Market conditions for deposits continued to be competitive during the quarter ended December 31, 2020; however, we continued lowering deposit rates, with the largest changes to our interest-bearing demand deposit and certificate of deposit rates being effective in second quarter of 2020. We expect to continue repricing high-rate certificates of deposits and letting those high cost deposits run-off when appropriate; such as when we are able to replace them with lower cost, core deposits.

Return on average assets (“ROA”) was 1.04% for the quarter ended December 31, 2020 compared to 0.95% and 1.31% for the quarters ended September 30, 2020 and December 31, 2019, respectively. ROA was impacted in the fourth quarter of 2020 and prior quarter in 2020 by increased provision for loan losses due to the economic uncertainties of the COVID-19 pandemic and loan growth. Pre-tax, pre-provision ROA* was 1.90% for the quarter ended December 31, 2020, compared to 1.72% for the quarter ended September 30, 2020, and 1.95% for the quarter ended December 31, 2019.

During the second and third quarters of 2020, significant focus was placed on helping the small businesses in our communities through the PPP. We are currently accepting applications for the third round of PPP loans which will begin funding in the first quarter of 2021. The PPP loans from the first and second rounds in 2020 have had a significant impact on our financial statements for the year ended December 31, 2020. These PPP loans along with those loans that fund in round three will continue to impact our results in the future. During the quarter ended December 31, 2020 we began receiving forgiveness payments from the SBA. Throughout this earnings release, we will address the impact, to the extent possible, of these loans including borrowings received through PPPLF to help fund these loans and to aid in liquidity, in addition to earnings and expenses related to these activities. Any estimated adjusted ratios that exclude the impact of this activity are non-GAAP measures. For more information about non-GAAP financial measures, please see the end of this earnings release.

The table below summarizes key information regarding the PPP loans as of the period indicated:

Original Loan Size As of December 31, 2020 $0.00 -

$50,000.00$50,0000.01 -

$150,000.00$150,000.01 -

$350,000.00$350,000.01 -

$2,000,000.00> 2,000,000.01 Totals (Dollars in thousands; unaudited) Principal outstanding: Existing customer $ 9,399 $ 22,614 $ 17,211 $ 55,821 $ 52,299 $ 157,344 New customer 18,324 30,325 34,206 64,591 61,052 208,498 Total principal outstanding 27,723 52,939 51,417 120,412 113,351 365,842 Deferred fees outstanding (906 ) (1,580 ) (1,538 ) (2,060 ) (631 ) (6,715 ) Deferred costs outstanding 487 208 114 86 17 912 Net deferred fees $ (419 ) $ (1,372 ) $ (1,424 ) $ (1,974 ) $ (614 ) $ (5,803 ) Total principal, net of deferred

fees$ 27,304 $ 51,567 $ 49,993 $ 118,438 $ 112,737 $ 360,039 Number of loans: Existing customer 434 263 81 77 13 868 New customer 1,006 344 161 90 19 1,620 Total loan count 1,440 607 242 167 32 2,488 Percent of total 57.9 % 24.4 % 9.7 % 6.7 % 1.3 % 100.0 % Forgiveness/Payoffs/Paydowns in Quarter Ended December 31, 2020, net Dollars $ 4,139 $ 9,330 $ 20,948 $ 52,587 $ - $ 87,004 Deferred fee recognized 114 470 826 1,254 119 2,783 The following table shows the Company’s key performance ratios for the periods indicated. The table also includes ratios that were adjusted by removing the impact of the PPP loans as described above. The adjusted ratios are non-GAAP measures. For more information about non-GAAP financial measures, see the end of this earnings release.

Three Months Ended Year ended (unaudited) December 31,

2020September 30,

2020June 30,

2020March 31,

2020December 31,

2019December 31,

2020December 31,

2019Return on average assets (1) 1.04 % 0.95 % 0.96 % 0.96 % 1.31 % 0.98 % 1.28 % Return on average equity (1) 13.36 % 12.14 % 11.37 % 8.66 % 11.66 % 11.44 % 11.29 % Pre-tax, pre-provision return

on average assets (1)(2)1.90 % 1.72 % 1.72 % 1.77 % 1.95 % 1.78 % 1.86 % Yield on earnings assets (1) 4.16 % 3.93 % 4.16 % 4.79 % 4.90 % 4.21 % 4.90 % Yield on loans receivable (1) 4.64 % 4.33 % 4.57 % 5.25 % 5.36 % 4.64 % 5.38 % Yield on loans receivable,

as adjusted (1)(2)5.00 % 4.78 % 4.94 % n/a n/a 4.99 % n/a Contractual yield on loans

receivable, excluding earned

fees (1)3.66 % 3.61 % 3.91 % 5.08 % 5.15 % 3.96 % 4.75 % Contractual yield on loans

receivable, excluding earned

fees and interest on PPP loans,

as adjusted (1)(2)4.65 % 4.69 % 4.84 % n/a n/a 4.80 % n/a Cost of funds (1) 0.29 % 0.33 % 0.41 % 0.70 % 0.70 % 0.40 % 0.73 % Cost of deposits (1) 0.22 % 0.27 % 0.35 % 0.64 % 0.63 % 0.35 % 0.65 % Net interest margin (1) 3.89 % 3.62 % 3.78 % 4.15 % 4.26 % 3.83 % 4.23 % Noninterest expense to average

assets (1)2.35 % 2.26 % 2.34 % 3.18 % 2.90 % 2.47 % 3.01 % Efficiency ratio 55.26 % 56.73 % 57.66 % 64.26 % 59.86 % 58.14 % 61.79 % Loans receivable to deposits 108.85 % 110.98 % 110.77 % 100.01 % 97.02 % 108.85 % 97.02 % (1) Annualized calculations shown for quarterly periods presented. (2) A reconciliation of the non-GAAP measures are set forth at the end of this earnings release. Noninterest income was $2.0 million in the fourth quarter of 2020, an increase of $107,000 from $1.9 million at the third quarter of 2020, and a decrease of $10,000 from $2.1 million in the fourth quarter of 2019. The increase over the prior quarter was primarily due to a $243,000 increase in loan referral fees that are earned when we originate a variable rate loan and arrange for the borrower to enter into an interest rate swap agreement with a third party to fix the interest rate for an extended period, a $159,000 increase in BaaS fees as a result of adding new relationships, and a $91,000 increase in mortgage broker fees, which are a result of increased production from the attractive low rate environment, partially offset by a decrease in other income due to the revaluation and write-down of an equity interest of $400,000. The $10,000 decrease over the quarter ended December 31, 2019 was primarily due to the revaluation and write-down of an equity interest of $400,000 recorded in other income, partially offset by $105,000 increase in mortgage broker fees, a $91,000 increase in loan referral fees, and a $79,000 increase in BaaS fees.

As of December 31, 2020, there were six active CCBX relationships, two CCBX relationships in the friends and family trials, three CCBX relationships in onboarding/implementation, four signed letters of intent for a CCBX relationship and a solid pipeline of potential new CCBX relationships. The following table illustrates the activity and growth in CCBX for the periods presented:

As of December 31, 2020 September 30, 2020 December 31, 2019 Active 6 4 2 Friends and family trials 2 1 0 Implementation / onboarding 3 4 3 Signed letters of intent 4 2 0 Total CCBX relationships 15 11 5 Total noninterest expense for the fourth quarter of 2020 increased to $10.5 million compared to $9.7 million for the preceding quarter and compared to $8.0 million for the fourth quarter of 2019. Noninterest expense variances for the quarter ended December 31, 2020, as compared to the quarter ended September 30, 2020, include a $66,000 increase in other expenses due to $65,000 increase in software license, maintenance and subscription expenses, which is expected to increase as we invest more in automated processing and as we grow product lines and our CCBX division. Salaries and employee benefits increased $462,000 for the quarter ended December 31, 2020 compared to $6.0 million for the quarter ended September 30, 2020, which is related to the hiring in our CCBX and CCDB divisions and additional staff for our ongoing banking growth initiatives. Legal and professional fees increased $203,000 due to CCBX division expenses and higher costs associated with legal and accounting work related to financial reporting. The increased expenses for the quarter ended December 31, 2020 compared to the fourth quarter in 2019 were largely due to a $1.5 million increase in salary expenses related to hiring staff for our CCBX division and additional staff for our ongoing banking growth initiatives. Other expenses increased $301,000 in the fourth quarter of 2020 compared to $692,000 for the quarter ended December 31, 2019, which is largely due to a $159,000 increase in software license, maintenance and subscription expenses, and a $74,000 increase in the provision for unfunded commitments. In addition, in the fourth quarter of 2020 compared to the fourth quarter of 2019, legal and professional fees increased $353,000 and Federal Deposit Insurance Corporation (“FDIC”) assessments increased $251,000. The increase in legal and professional expenses is associated with CCBX division expenses and higher costs associated with legal and accounting work related to financial reporting. The increase in FDIC assessments is primarily the result of a credit issued to the Bank for assessments in the quarter ended December 31, 2019, combined with an increase in deposits compared to the quarter ended December 31, 2019.

The provision for income taxes was $1.2 million at December 31, 2020, a $150,000 increase compared to $1.1 million for the third quarter of 2020 and a $285,000 increase compared to $947,000 for the fourth quarter of 2019, both as a result of increased taxable income. The Company uses a federal statutory tax rate of 21% as a basis for calculating provision for income taxes.

Financial Condition

Total assets increased $16.5 million, or 0.9%, to $1.77 billion at December 31, 2020 compared to $1.75 billion at September 30, 2020. The primary cause of the increase was $37.7 million in increased loans receivable, as a result of overall growth in the loan portfolio, partially offset by a $23.9 million decrease in interest earning deposits with other banks. Total assets increased $637.6 million, or 56.5% at December 31, 2020, compared to $1.13 billion at December 31, 2019. This increase was largely the result of a $608.0 million increase in loans receivable, which includes $365.8 million in PPP loans as of December 31, 2020, combined with a $32.9 million increase in interest earning deposits with other banks.

Total loans receivable increased $37.7 million to $1.55 billion at December 31, 2020, from $1.51 billion at September 30, 2020, and increased $608.0 million from $939.1 million at December 31, 2019. The growth in loans receivable over the quarter ended September 30, 2020 was due primarily to growth in non-PPP loans of $122.0 million consisting of an increase of $69.7 million in commercial real estate loans, $37.0 million in other commercial and industrial loans, and $22.7 million in residential real estate loans, partially offset by a decrease of $87.0 million in PPP loans. Total loans receivable is net of $9.2 million in net deferred origination fees, $5.8 million of which is attributed to PPP loans. Deferred fees on PPP loans are earned over the life of the loan, with a maximum maturity of five years. As of December 31, 2020, 55.2% of the total $12.9 million in net deferred fees on the first and second rounds of PPP loans was fully earned. The increase in loans receivable over the quarter ended December 31, 2019 was due to a $365.8 million increase in PPP loans, and $248.0 million increase in non-PPP loans consisting of $161.5 million increase in commercial real estate loans, $62.0 million in other commercial and industrial loans and $28.9 million in residential real estate loans.

The second round of the PPP program closed to new loan applicants on August 8, 2020, and since that time we have been accepting applications from customers for loan forgiveness. As of December 31, 2020, we have received $87.0 million in forgiveness payments or principal paydowns, on 472 loans. We expect that the pace of forgiveness will increase in the first half of 2021. Forgiveness of principal, early paydowns and payoffs on PPP loans will increase interest income earned in those periods from the recognition of deferred PPP loan fees. Customers with two-year loans are also able to request that their PPP loan be extended to a five year maturity, which we anticipate may be a good option for customers not eligible for forgiveness.

The third round of PPP loans opened to applicants on January 19, 2021. We expect to again accept and process applications for both existing and new customers, to help small businesses in our communities. As of January 25, 2021, we have accepted applications for $233.6 million, representing 1,385 new and existing customers, in the third round of the PPP program.

The following table summarizes the loan portfolio at the periods indicated.

As of December 31, 2020 September 30, 2020 December 31, 2019 (Dollars in thousands; unaudited) Balance % to Total Balance % to Total Balance % to Total Commercial and industrial loans: PPP loans $ 365,842 23.5 % $ 452,846 29.8 % $ - 0.0 % All other commercial &

industrial loans173,358 11.0 136,358 8.9 111,401 11.8 Real estate loans: Construction, land and

land development loans94,423 6.1 100,955 6.6 97,034 10.3 Residential real estate loans 143,869 9.3 121,147 8.0 115,011 12.2 Commercial real estate loans 774,925 49.8 705,186 46.4 613,398 65.2 Consumer and other loans 3,916 0.3 3,927 0.3 4,214 0.5 Gross loans receivable 1,556,333 100.0 % 1,520,419 100.0 % 941,058 100.0 % Net deferred origination fees -

PPP loans(5,803 ) (8,586 ) - Net deferred origination fees -

Other loans(3,392 ) (2,444 ) (1,955 ) Loans receivable $ 1,547,138 $ 1,509,389 $ 939,103 Please see Appendix A for additional loan portfolio detail regarding industry concentrations in response to the volatile economic environment due to the COVID-19 pandemic.

Total deposits increased $61.3 million, or 4.5%, to $1.42 billion at December 31, 2020 from $1.36 billion at September 30, 2020. The increase is largely due to a $57.9 million increase in core deposits, which is primarily the result of expanding and growing banking relationships with new customers, including deposit relationships from PPP loans made to noncustomers, who moved their banking relationship to the Bank. During the quarter ended December 31, 2020, noninterest bearing deposits increased $21.6 million, or 3.8%, to $592.3 million from $570.7 million at September 30, 2020. Included in the increase in noninterest bearing deposits is an increase in CCBX deposits of $11.9 million for the quarter ended December 31, 2020. In the fourth quarter of 2020 compared to the quarter ended September 30, 2020, NOW and money market accounts increased $33.4 million, and savings accounts increased $2.9 million. BaaS-brokered deposits increased $8.6 million, and time deposits decreased $5.3 million. Total deposits increased $453.3 million, or 46.8%, to $1.42 billion at December 31, 2020 compared to $968.0 million at December 31, 2019. Noninterest bearing deposits increased $221.0 million, or 59.5%, to $592.3 million at December 31, 2020 from $371.2 million at December 31, 2019. NOW and money market accounts increased $220.4 million, or 50.3%, to $658.3 million at December 31, 2020, and savings accounts increased $24.3 million and BaaS-brokered deposits increased $9.9 million while time deposits decreased $22.2 million. Efforts to retain and grow core deposits are evidenced by the high ratios in these categories when compared to total deposits.

The following table summarizes the deposit portfolio at the periods indicated.

As of December 31, 2020 September 30, 2020 December 31, 2019 (Dollars in thousands, unaudited) Balance % to Total Balance % to Total Balance % to Total Demand, noninterest bearing $ 592,261 41.7 % $ 570,664 42.0 % $ 371,243 38.4 % NOW and money market 658,323 46.3 624,891 45.9 437,908 45.2 Savings 77,611 5.4 74,694 5.5 53,365 5.5 Total core deposits 1,328,195 93.4 1,270,249 93.4 862,516 89.1 BaaS-brokered deposits 33,482 2.4 24,870 1.8 23,586 2.4 Time deposits less than $250,000 41,145 2.9 41,676 3.1 51,644 5.4 Time deposits $250,000 and over 18,485 1.3 23,216 1.7 30,213 3.1 Total deposits $ 1,421,307 100.0 % $ 1,360,011 100.0 % $ 967,959 100.0 % To support and promote the effectiveness of the SBA PPP loan program, the Federal Reserve is supplying liquidity to participating financial institutions through non-recourse term financing secured by PPP loans to small businesses. The PPPLF extends low cost borrowing lines, 0.35% interest rate, to eligible financial institutions that originate PPP loans, taking the loans as collateral at face value. Borrowings are required to be paid down as the pledged PPP loans are paid down. As of December 31, 2020, there was $153.7 million in outstanding PPPLF advances and pledged PPP loans, compared to $202.6 million at September 30, 2020. The PPPLF program is currently available for new borrowings until March 31, 2021.

The Federal Home Loan Bank (“FHLB”) allows us to borrow against our line of credit, which is collateralized by certain loans. As of December 31, 2020, we borrowed a total of $25.0 million in FHLB medium term advances. This includes a $10.0 million advance with a remaining term of 2.25 years and $15.0 million advance with a remaining term of 4.25 years. These advances provide an alternative and stable source of funding for loan demand. Although there are no immediate plans to borrow additional funds, additional FHLB borrowing capacity of $65.7 million was available under this arrangement as of December 31, 2020.

Total shareholders’ equity increased $5.0 million since September 30, 2020. The increase in shareholders’ equity was primarily due to $4.7 million in net earnings for the three months ended December 31, 2020.

Capital Ratios

The Company and the Bank remain well capitalized at December 31, 2020, as summarized in the following table.

Capital Ratios: Coastal

Community

BankCoastal

Financial

CorporationFinancial

Institution Basel

III Regulatory

Guidelines(unaudited) Tier 1 leverage capital 9.29 % 9.05 % 5.00 % Adjusted Tier 1 leverage capital ratio, excluding PPP loans (1) 10.91 % 10.63 % 5.00 % Common Equity Tier 1 risk-based capital 11.86 % 11.27 % 6.50 % Tier 1 risk-based capital 11.86 % 11.55 % 8.00 % Total risk-based capital 13.11 % 13.61 % 10.00 % (1) A reconciliation of the non-GAAP measure is set forth at the end of this earnings release. As previously disclosed, during the quarter ended March 31, 2020, the Company contributed $7.5 million in capital to the Bank due to the volatile economic environment. No additional contributions have been made; however, the Company could downstream additional funds to the Bank in the future, if necessary.

Asset Quality

The allowance for loan losses was $19.3 million and 1.25% of loans receivable at December 31, 2020 compared to $17.0 million and 1.13% at September 30, 2020 and $11.5 million and 1.22% at December 31, 2019. At December 31, 2020, there was $365.8 million in PPP loans, which are 100% guaranteed by the SBA. Excluding PPP loans, the allowance for loan losses to loans receivable* would be 1.62% for the quarter ended December 31, 2020. Provision for loan losses totaled $2.6 million for the three months ended December 31, 2020, $2.2 million for the three months ended September 30, 2020, and $820,000 for the three months ended December 31, 2019. Net charge-offs totaled $384,000 for the quarter ended December 31, 2020, compared to $1,000 for the quarter ended September 30, 2020 and $238,000 for the quarter ended December 31, 2019. Net charge-offs for the quarter ended December 31, 2020 primarily included a charge-off for $368,000 to secure a payoff of a $3.3 million longer-term nonperforming loan from the portfolio.

The Company’s provision for loan losses during the quarters ended December 31, 2020, September 30, 2020, June 30, 2020 and March 31, 2020, is related to an increase in qualitative factors related to the economic uncertainties caused by the COVID-19 pandemic and loan growth. The Company is not required to implement the provisions of the Current Expected Credit Loss accounting standard until January 1, 2023 and will continue to account for the allowance for credit losses under the incurred loss model.

At December 31, 2020, our nonperforming assets were $712,000, or 0.04% of total assets, compared to $4.5 million, or 0.26%, of total assets at September 30, 2020, and $1.0 million, or 0.09%, of total assets at December 31, 2019. Nonperforming assets decreased $3.8 million during the quarter ended December 31, 2020, compared to the quarter ended September 30, 2020, with the pay-off and partial charge-off of one loan ($3.3 million) and principal pay-downs and pay-offs on other loans.

Management is continuing to actively monitor the loan portfolio to identify borrowers experiencing difficulties with repayment and are proactively working with them to reduce potential losses through the prudent use of PPP loans, deferrals, and modifications in accordance with regulatory guidelines. There were no repossessed assets or other real estate owned at December 31, 2020. Our nonperforming loans to loans receivable ratio was 0.05% at December 31, 2020, compared to 0.30% at September 30, 2020, and 0.11% at December 31, 2019. Nonperforming loans totaled $712,000 at December 31, 2020, compared to $4.5 million at September 30, 2020. The decrease of $3.8 million in the quarter ended December 31, 2020, compared to the quarter ended September 30, 2020 was largely due to one nonperforming construction, land and land development loan for $3.3 million that was paid-off and included a partial charge-off of $368,000. These changes, combined with other pay-offs and principal reductions, resulted an overall decrease in our ratio of nonperforming loans to loans receivable and nonperforming loans to total assets compared to September 30, 2020.

To date we have not seen a significant change in our credit quality metrics, as demonstrated by the low level of charge-offs and nonperforming loans for the year ended December 31, 2020. The long-term economic impact of the COVID-19 pandemic, political gridlock, trade issues, and decline in oil prices is unknown; however, the Company remains diligent in its efforts to communicate and proactively work with borrowers to help mitigate potential credit deterioration.

Pursuant to federal guidance, the Company deferred and/or modified payments on loans to assist customers financially during the COVID-19 pandemic and economic shutdown. A total of $233.9 million in loans were deferred and/or modified under this guidance during the second, third and fourth quarters of 2020. All of the loans that were on deferred and/or modified status as of the quarter ended September 30, 2020 have either successfully returned to active status or have closed. All of these loans are current, with no loans more than 30 days past due as of December 31, 2020. For the quarter ended December 31, 2020, three loans, or $9.3 million remained on deferred and/or modified status. The purpose of this program is to provide cash flow relief for small business customers as they navigate through the uncertainties of the COVID-19 pandemic. The Company’s deferral program has been successful as evidenced by customers’ ability to migrate from deferral to active status and resume making payments as planned.

The following table details the Company’s nonperforming assets for the periods indicated.

As of December 31, September 30, December 31, (Dollars in thousands, unaudited) 2020 2020 2019 Nonaccrual loans: Commercial and industrial loans $ 537 $ 625 $ 965 Real estate: Construction, land and land development - 3,269 - Residential real estate 175 178 65 Commercial real estate - 405 - Total nonaccrual loans 712 4,477 1,030 Accruing loans past due 90 days or more: Total accruing loans past due 90 days or more - - - Total nonperforming loans 712 4,477 1,030 Other real estate owned - - - Repossessed assets - - - Total nonperforming assets $ 712 $ 4,477 $ 1,030 Troubled debt restructurings, accruing - - - Total nonperforming loans to loans receivable 0.05 % 0.30 % 0.11 % Total nonperforming assets to total assets 0.04 % 0.26 % 0.09 % ____

* A reconciliation of the non-GAAP measures are set forth at the end of this earnings release.About Coastal Financial

Coastal Financial Corporation (Nasdaq: CCB) (the “Company”), is an Everett, Washington based bank holding company whose wholly owned subsidiaries are Coastal Community Bank (“Bank”) and Arlington Olympic LLC. The $1.8 billion community bank that the Bank operates provides service through 15 branches in Snohomish, Island, and King Counties, the Internet and its mobile banking application. The Bank provides banking as a service to broker dealers and digital financial service providers through its CCBX Division. In 2021, the Bank expects to introduce CCDB, its digital bank division in collaboration with Google. To learn more about Coastal visit www.coastalbank.com.

Contact

Eric Sprink, President & Chief Executive Officer, (425) 357-3659

Joel Edwards, Executive Vice President & Chief Financial Officer, (425) 357-3687Forward-Looking Statements

This earnings release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. Any statements about our management’s expectations, beliefs, plans, predictions, forecasts, objectives, assumptions or future events or performance are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words or phrases such as “anticipate,” “believes,” “can,” “could,” “may,” “predicts,” “potential,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “intends” and similar words or phrases. Any or all of the forward-looking statements in this earnings release may turn out to be inaccurate. The inclusion of or reference to forward-looking information in this earnings release should not be regarded as a representation by us or any other person that the future plans, estimates or expectations contemplated by us will be achieved. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of risks, uncertainties and assumptions that are difficult to predict. Factors that could cause actual results to differ materially from those in the forward-looking statements include, without limitation, the risks and uncertainties discussed under “Risk Factors” in our Annual Report on Form 10-K for the most recent period filed, our Quarterly Report on Form 10-Q for the most recent quarter, and in any of our subsequent filings with the Securities and Exchange Commission.

If one or more events related to these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may differ materially from what we anticipate. You are cautioned not to place undue reliance on forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made and we undertake no obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as required by law.

COASTAL FINANCIAL CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF FINANCIAL CONDITION

(Dollars in thousands; unaudited)ASSETS December 31, September 30, December 31, 2020 2020 2019 Cash and due from banks $ 18,965 $ 14,136 $ 16,555 Interest earning deposits with other banks 144,152 168,034 111,259 Investment securities, available for sale, at fair value 20,399 20,428 28,360 Investment securities, held to maturity, at amortized cost 2,848 3,354 4,350 Other investments 6,059 5,951 4,505 Loans receivable 1,547,138 1,509,389 939,103 Allowance for loan losses (19,262 ) (17,046 ) (11,470 ) Total loans receivable, net 1,527,876 1,492,343 927,633 Premises and equipment, net 17,108 16,881 13,108 Operating lease right-of-use assets 7,120 7,379 8,493 Accrued interest receivable 8,616 8,216 2,980 Bank-owned life insurance, net 7,082 7,031 6,882 Deferred tax asset, net 3,799 2,722 2,743 Other assets 2,098 3,144 1,658 Total assets $ 1,766,122 $ 1,749,619 $ 1,128,526 LIABILITIES AND SHAREHOLDERS’ EQUITY LIABILITIES Deposits $ 1,421,307 $ 1,360,011 $ 967,959 Federal Home Loan Bank advances 24,999 24,999 10,000 Paycheck Protection Program Liquidity Facility 153,716 202,595 - Subordinated debt, net 9,993 9,989 9,979 Junior subordinated debentures, net 3,584 3,584 3,583 Deferred compensation 863 891 974 Accrued interest payable 531 481 308 Operating lease liabilities 7,323 7,579 8,679 Other liabilities 3,589 4,258 2,871 Total liabilities 1,625,905 1,614,387 1,004,353 SHAREHOLDERS’ EQUITY Common stock 87,815 87,479 86,983 Retained earnings 52,368 47,707 37,222 Accumulated other comprehensive income (loss), net of tax 34 46 (32 ) Total shareholders’ equity 140,217 135,232 124,173 Total liabilities and shareholders’ equity $ 1,766,122 $ 1,749,619 $ 1,128,526 COASTAL FINANCIAL CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

(Dollars in thousands, except per share amounts; unaudited)Three Months Ended December 31, September 30, December 31, 2020 2020 2019 INTEREST AND DIVIDEND INCOME Interest and fees on loans $ 17,885 $ 16,244 $ 12,323 Interest on interest earning deposits with other banks 76 99 477 Interest on investment securities 31 27 154 Dividends on other investments 106 24 80 Total interest and dividend income 18,098 16,394 13,034 INTEREST EXPENSE Interest on deposits 758 880 1,511 Interest on borrowed funds 407 418 192 Total interest expense 1,165 1,298 1,703 Net interest income 16,933 15,096 11,331 PROVISION FOR LOAN LOSSES 2,600 2,200 820 Net interest income after provision for loan losses 14,333 12,896 10,511 NONINTEREST INCOME Deposit service charges and fees 867 824 805 BaaS fees 735 576 656 Loan referral fees 423 180 332 Mortgage broker fees 216 125 111 Sublease and lease income 31 30 27 Gain on sales of loans, net 35 47 - Other (258 ) 160 128 Total noninterest income 2,049 1,942 2,059 NONINTEREST EXPENSE Salaries and employee benefits 6,433 5,971 4,901 Occupancy 1,026 1,091 972 Data processing 599 577 544 Director and staff expenses 187 156 302 Excise taxes 301 291 190 Marketing 37 52 93 Legal and professional fees 584 381 231 Federal Deposit Insurance Corporation assessments 230 148 (21 ) Business development 99 72 111 Other 993 927 692 Total noninterest expense 10,489 9,666 8,015 Income before provision for income taxes 5,893 5,172 4,555 PROVISION FOR INCOME TAXES 1,232 1,082 947 NET INCOME $ 4,661 $ 4,090 $ 3,608 Basic earnings per common share $ 0.39 $ 0.34 $ 0.30 Diluted earnings per common share $ 0.38 $ 0.34 $ 0.30 Weighted average number of common shares outstanding: Basic 11,936,289 11,919,850 11,903,750 Diluted 12,280,191 12,181,272 12,213,512 COASTAL FINANCIAL CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

(Dollars in thousands, except per share amounts; unaudited)Year ended December 31, December 31, 2020 2019 INTEREST AND DIVIDEND INCOME Interest and fees on loans $ 61,910 $ 45,350 Interest on interest earning deposits with other banks 663 2,423 Interest on investment securities 230 635 Dividends on other investments 235 179 Total interest and dividend income 63,038 48,587 INTEREST EXPENSE Interest on deposits 4,288 5,802 Interest on borrowed funds 1,364 774 Total interest expense 5,652 6,576 Net interest income 57,386 42,011 PROVISION FOR LOAN LOSSES 8,308 2,544 Net interest income after provision for loan losses 49,078 39,467 NONINTEREST INCOME Deposit service charges and fees 3,091 3,107 BaaS fees 2,365 2,060 Loan referral fees 1,726 1,438 Mortgage broker fees 655 447 Sublease and lease income 122 58 Gain on sales of loans, net 82 490 Gain on sales of securities, net - 171 Other 141 487 Total noninterest income 8,182 8,258 NONINTEREST EXPENSE Salaries and employee benefits 23,302 18,959 Occupancy 3,977 3,775 Data processing 2,348 2,081 Director and staff expenses 800 1,000 Excise taxes 1,057 719 Marketing 317 393 Legal and professional fees 1,762 1,103 Federal Deposit Insurance Corporation assessments 522 184 Business development 344 431 Other 3,690 2,418 Total noninterest expense 38,119 31,063 Income before provision for income taxes 19,141 16,662 PROVISION FOR INCOME TAXES 3,995 3,461 NET INCOME $ 15,146 $ 13,201 Basic earnings per common share $ 1.27 $ 1.11 Diluted earnings per common share $ 1.24 $ 1.08 Weighted average number of common shares outstanding: Basic 11,920,735 11,896,258 Diluted 12,209,371 12,196,120 COASTAL FINANCIAL CORPORATION

AVERAGE BALANCES, YIELDS, AND RATES – QUARTERLY

(Dollars in thousands; unaudited)For the Three Months Ended December 31, 2020 September 30, 2020 December 31, 2019 Average Interest & Yield / Average Interest & Yield / Average Interest & Yield / Balance Dividends Cost (4) Balance Dividends Cost (4) Balance Dividends Cost (4) Assets Interest earning assets: Interest earning deposits $ 166,744 $ 76 0.18 % $ 137,568 $ 99 0.29 % $ 106,985 $ 477 1.77 % Investment securities (1) 23,730 31 0.52 23,882 27 0.45 32,871 154 1.86 Other Investments 6,124 106 6.89 5,951 24 1.60 3,743 80 8.48 Loans receivable (2) 1,533,533 17,885 4.64 1,493,024 16,244 4.33 911,373 12,323 5.36 Total interest earning assets 1,730,131 18,098 4.16 1,660,425 16,394 3.93 1,054,972 13,034 4.90 Noninterest earning assets: Allowance for loan losses (17,767 ) (15,711 ) (11,002 ) Other noninterest earning assets 62,359 60,160 51,373 Total assets $ 1,774,723 $ 1,704,874 $ 1,095,343 Liabilities and Shareholders’ Equity Interest bearing liabilities: Interest bearing deposits $ 808,351 $ 758 0.37 % $ 750,790 $ 880 0.47 % $ 585,277 $ 1,511 1.02 % Subordinated debt, net 9,991 148 5.89 9,987 148 5.90 9,977 148 5.89 Junior subordinated debentures, net 3,584 22 2.44 3,584 23 2.55 3,583 39 4.32 PPPLF borrowings 188,222 166 0.35 199,076 176 0.35 - - 0.00 FHLB advances and other borrowings 25,001 71 1.13 24,999 71 1.13 893 5 2.22 Total interest bearing liabilities 1,035,149 1,165 0.45 988,436 1,298 0.52 599,730 1,703 1.13 Noninterest bearing deposits 588,764 569,615 360,030 Other liabilities 11,968 12,781 12,869 Total shareholders' equity 138,842 134,042 122,714 Total liabilities and shareholders' equity $ 1,774,723 $ 1,704,874 $ 1,095,343 Net interest income $ 16,933 $ 15,096 $ 11,331 Interest rate spread 3.71 % 3.41 % 3.77 % Net interest margin (3) 3.89 % 3.62 % 4.26 % (1) For presentation in this table, average balances and the corresponding average rates for investment securities are based upon historical cost, adjusted

for amortization of premiums and accretion of discounts.(2) Includes nonaccrual loans. (3) Net interest margin represents net interest income divided by the average total interest earning assets. (4) Yields and costs are annualized. COASTAL FINANCIAL CORPORATION

AVERAGE BALANCES, YIELDS, AND RATES – YEAR-TO-DATE

(Dollars in thousands; unaudited)For the Year Ended December 31, 2020 December 31, 2019 Average Interest & Yield / Average Interest & Yield / Balance Dividends Cost Balance Dividends Cost Assets Interest earning assets: Interest earning deposits $ 133,951 $ 663 0.49 % $ 107,916 $ 2,423 2.25 % Investment securities (1) 24,120 230 0.95 37,368 635 1.70 Other Investments 5,608 235 4.19 3,545 179 5.05 Loans receivable (2) 1,333,028 61,910 4.64 843,450 45,350 5.38 Total interest earning assets $ 1,496,707 $ 63,038 4.21 $ 992,279 $ 48,587 4.90 Noninterest earning assets: Allowance for loan losses (14,686 ) (10,304 ) Other noninterest earning assets 58,970 49,998 Total assets $ 1,540,991 $ 1,031,973 Liabilities and Shareholders’ Equity Interest bearing liabilities: Interest bearing deposits $ 724,279 $ 4,288 0.59 % $ 565,713 $ 5,802 1.03 % Subordinated debt, net 9,986 589 5.90 9,971 587 5.89 Junior subordinated debentures, net 3,584 105 2.93 3,582 168 4.69 PPPLF borrowings 124,068 435 0.35 - - 0.00 FHLB advances and other borrowings 20,736 235 1.13 819 19 2.32 Total interest bearing liabilities $ 882,653 $ 5,652 0.64 $ 580,085 $ 6,576 1.13 Noninterest bearing deposits 513,550 322,064 Other liabilities 12,445 12,944 Total shareholders' equity 132,343 116,880 Total liabilities and shareholders' equity $ 1,540,991 $ 1,031,973 Net interest income $ 57,386 $ 42,011 Interest rate spread 3.57 % 3.76 % Net interest margin (3) 3.83 % 4.23 % (1) For presentation in this table, average balances and the corresponding average rates for investment securities are based upon historical cost, adjusted for amortization of premiums and accretion of discounts. (2) Includes nonaccrual loans. (3) Net interest margin represents net interest income divided by the average total interest earning assets. COASTAL FINANCIAL CORPORATION

QUARTERLY STATISTICS

(Dollars in thousands, except share and per share data; unaudited)Three Months Ended December 31, September 30, June 30, March 31, December 31, 2020 2020 2020 2020 2019 Income Statement Data: Interest and dividend income $ 18,098 $ 16,394 $ 15,426 $ 13,120 $ 13,034 Interest expense 1,165 1,298 1,433 1,756 1,703 Net interest income 16,933 15,096 13,993 11,364 11,331 Provision for loan losses 2,600 2,200 1,930 1,578 820 Net interest income after provision for loan losses 14,333 12,896 12,063 9,786 10,511 Noninterest income 2,049 1,942 1,520 2,671 2,059 Noninterest expense 10,489 9,666 8,945 9,019 8,015 Net income - pre-tax, pre-provision (1) 8,493 7,372 6,568 5,016 5,375 Provision for income tax 1,232 1,082 967 714 947 Net income 4,661 4,090 3,671 2,724 3,608 As of and for the Three Month Period December 31, September 30, June 30, March 31, December 31, 2020 2020 2020 2020 2019 Balance Sheet Data: Cash and cash equivalents $ 163,117 $ 182,170 $ 174,176 $ 129,236 $ 127,814 Investment securities 23,247 23,782 24,318 19,759 32,710 Loans receivable 1,547,138 1,509,389 1,447,144 1,005,180 939,103 Allowance for loan losses (19,262 ) (17,046 ) (14,847 ) (12,925 ) (11,470 ) Total assets 1,766,122 1,749,619 1,678,956 1,184,071 1,128,526 Interest bearing deposits 829,046 789,347 742,633 659,559 596,716 Noninterest bearing deposits 592,261 570,664 563,794 345,503 371,243 Core deposits (2) 1,328,195 1,270,249 1,212,215 892,408 862,516 Total deposits 1,421,307 1,360,011 1,306,427 1,005,062 967,959 Total borrowings 192,292 241,167 228,725 38,564 23,562 Total shareholders’ equity 140,217 135,232 130,977 127,166 124,173 Share and Per Share Data (3): Earnings per share – basic $ 0.39 $ 0.34 $ 0.31 $ 0.23 $ 0.30 Earnings per share – diluted $ 0.38 $ 0.34 $ 0.30 $ 0.22 $ 0.30 Dividends per share - - - - - Book value per share (4) $ 11.73 $ 11.34 $ 10.98 $ 10.66 $ 10.42 Tangible book value per share (5) $ 11.73 $ 11.34 $ 10.98 $ 10.66 $ 10.42 Weighted avg outstanding shares – basic 11,936,289 11,919,850 11,917,394 11,909,248 11,903,750 Weighted avg outstanding shares – diluted 12,280,191 12,181,272 12,190,284 12,208,175 12,213,512 Shares outstanding at end of period 11,954,327 11,930,243 11,926,263 11,929,413 11,913,885 Stock options outstanding at end of period 749,397 769,607 774,587 774,937 784,217 As of and for the Three Month Period December 31, September 30, June 30, March 31, December 31, 2020 2020 2020 2020 2019 Credit Quality Data: Nonperforming assets to total assets 0.04 % 0.26 % 0.26 % 0.06 % 0.09 % Nonperforming assets to loans receivable and OREO 0.05 % 0.30 % 0.31 % 0.08 % 0.11 % Nonperforming loans to total loans receivable 0.05 % 0.30 % 0.31 % 0.08 % 0.11 % Allowance for loan losses to nonperforming loans 2705.3 % 380.7 % 334.8 % 1694.0 % 1113.6 % Allowance for loan losses to total loans receivable 1.25 % 1.13 % 1.03 % 1.29 % 1.22 % Allowance for loan losses to loans receivable, as adjusted (1) 1.62 % 1.60 % 1.46 % n/a n/a Gross charge-offs $ 386 $ 2 $ 13 $ 124 $ 242 Gross recoveries $ 2 $ 1 $ 5 $ 1 $ 4 Net charge-offs to average loans (6) 0.10 % 0.00 % 0.00 % 0.05 % 0.10 % Capital Ratios (7): Tier 1 leverage capital 9.05 % 9.20 % 9.38 % 11.43 % 11.64 % Common equity Tier 1 risk-based capital 11.27 % 12.14 % 12.34 % 12.10 % 12.74 % Tier 1 risk-based capital 11.55 % 12.45 % 12.67 % 12.43 % 13.10 % Total risk-based capital 13.61 % 14.61 % 14.88 % 14.65 % 15.35 % (1) A reconciliation of the non-GAAP measures are set forth at the end of this earnings release. (2) Core deposits are defined as all deposits excluding BaaS-brokered and all time deposits. (3) Share and per share amounts are based on total common shares outstanding. (4) We calculate book value per share as total shareholders’ equity at the end of the relevant period divided by the outstanding number of our common shares at the end of each period. (5) Tangible book value per share is a non-GAAP financial measure. We calculate tangible book value per share as total shareholders’ equity at the end of the relevant period, less goodwill and other intangible assets, divided by the outstanding number of our common shares at the end of each period. The most directly comparable GAAP financial measure is book value per share. We had no goodwill or other intangible assets as of any of the dates indicated. As a result, tangible book value per share is the same as book value per share as of each of the dates indicated. (6) Annualized calculations. (7) Capital ratios are for the Company, Coastal Financial Corporation. Non-GAAP Financial Measures

The Company uses certain non-GAAP financial measures to provide meaningful supplemental information regarding the Company’s operational performance and to enhance investors’ overall understanding of such financial performance. However, these non-GAAP financial measures are supplemental and are not a substitute for an analysis based on GAAP measures. As other companies may use different calculations for these adjusted measures, this presentation may not be comparable to other similarly titled adjusted measures reported by other companies.

The following non-GAAP measures are presented to illustrate the impact of provision for loan losses and provision for income taxes on net income and return on average assets.

Pre-tax, pre-provision net income is a non-GAAP measure that excludes the impact of provision for loan losses and provision for income taxes from net income. The most directly comparable GAAP measure is net income.

Pre-tax, pre-provision return on average assets is a non-GAAP measure that excludes the impact of provision for loan losses and provision for income taxes from return on average assets. The most directly comparable GAAP measure is return on average assets.

Reconciliations of the GAAP and non-GAAP measures are presented below.

As of and for the

Three Months EndedAs of and for the

Years Ended(Dollars in thousands, unaudited) December 31,

2020September 30,

2020June 30,

2020March 31,

2020December 31,

2019December 31,

2020December 31,

2019Pre-tax, pre-provision net income and pre-tax, pre-provision return on average assets: Total average assets $ 1,774,723 $ 1,704,874 $ 1,538,546 $ 1,141,453 $ 1,095,343 $ 1,540,991 $ 1,031,973 Total net income 4,661 4,090 3,671 2,724 3,608 15,146 13,201 Plus: provision for loan

losses2,600 2,200 1,930 1,578 820 8,308 2,544 Plus: provision for

income taxes1,232 1,082 967 714 947 3,995 3,461 Pre-tax, pre-provision net

income$ 8,493 $ 7,372 $ 6,568 $ 5,016 $ 5,375 $ 27,449 $ 19,206 Return on average assets 1.04 % 0.95 % 0.96 % 0.96 % 1.31 % 0.98 % 1.28 % Pre-tax, pre-provision

return on average

assets:1.90 % 1.72 % 1.72 % 1.77 % 1.95 % 1.78 % 1.86 % The following non-GAAP financial measures are presented to illustrate and identify the impact of PPP loans on loans receivable related measures. By removing these significant items and showing what the results would have been without them, we are providing investors with the information to better compare results with periods that did not have these significant items. These measures include the following:

Adjusted allowance for loan losses to loans receivable is a non-GAAP measure that excludes the impact of PPP loans on balance sheet. The most directly comparable GAAP measure is allowance for loan losses to loans receivable.

Adjusted yield on loans receivable is a non-GAAP measure that excludes the impact of PPP loans on balance sheet. The most directly comparable GAAP measure is yield on loans.

Adjusted contractual yield on loans receivable, excluding earned fees and interest on PPP loans is a non-GAAP measure that excludes the impact of PPP loans on balance sheet. The most directly comparable GAAP measure is contractual yield on loans, excluding fees.

Adjusted Tier 1 leverage capital ratio, excluding PPP loans is a non-GAAP measure that excludes the impact of PPP loans on balance sheet. The most directly comparable GAAP measure is Tier 1 leverage capital ratio.

Reconciliations of the GAAP and non-GAAP measures are presented below.

Three Months Ended Year Ended (Dollars in thousands, unaudited) December 31, 2020 September 30, 2020 December 31, 2020 Adjusted allowance for loan losses to loans receivable: Total loans, net of deferred fees $ 1,547,138 $ 1,509,389 $ 1,547,138 Less: PPP loans (365,842 ) (452,846 ) (365,842 ) Less: net deferred fees on PPP loans 5,803 8,586 5,803 Adjusted loans, net of deferred fees $ 1,187,099 $ 1,065,129 $ 1,187,099 Allowance for loan losses $ (19,262 ) $ (17,046 ) $ (19,262 ) Allowance for loan losses to loans receivable 1.25 % 1.13 % 1.25 % Adjusted allowance for loan losses to loans receivable 1.62 % 1.60 % 1.62 % Adjusted yield on loans receivable: Total average loans receivable $ 1,533,533 $ 1,493,024 $ 1,333,028 Less: average PPP loans (424,290 ) (448,313 ) (302,685 ) Plus: average deferred fees on PPP loans 7,385 9,599 6,432 Adjusted total average loans receivable $ 1,116,628 $ 1,054,310 $ 1,036,775 Interest income on loans $ 17,885 $ 16,244 $ 61,910 Less: interest and deferred fee income

recognized on PPP loans(3,847 ) (3,566 ) (10,172 ) Adjusted interest income on loans $ 14,038 $ 12,678 $ 51,738 Yield on loans receivable 4.64 % 4.33 % 4.64 % Adjusted yield on loans receivable: 5.00 % 4.78 % 4.99 % Adjusted contractual yield on loans receivable, excluding earned fees and interest on PPP loans: Total average loans receivable $ 1,533,533 $ 1,493,024 $ 1,333,028 Less: average PPP loans (424,290 ) (448,313 ) (302,685 ) Plus: average deferred fees on PPP loans $ 7,385 $ 9,599 $ 6,432 Adjusted total average loans receivable,

excluding earned fees$ 1,116,628 $ 1,054,310 $ 1,036,775 Interest and earned fee income on loans $ 17,885 $ 16,244 $ 61,910 Less: earned fee income on all loans $ (3,762 ) $ (2,693 ) $ (9,065 ) Less: interest income on PPP loans (1,064 ) (1,129 ) (3,030 ) Adjusted interest income on loans $ 13,059 $ 12,422 $ 49,815 Contractual yield on loans receivable,

excluding earned fees3.66 % 3.61 % 3.96 % Adjusted contractual yield on loans receivable,

excluding earned fees and interest on PPP loans:4.65 % 4.69 % 4.80 % (Dollars in thousands, unaudited) As of

December 31, 2020Adjusted Tier 1 leverage capital ratio, excluding PPP loans: Company: Tier 1 capital $ 143,532 Average assets for the leverage capital ratio $ 1,586,350 Less: Average PPP loans (424,290 ) Plus: Average PPPLF borrowings 188,222 Adjusted average assets for the leverage capital ratio $ 1,350,282 Tier 1 leverage capital ratio 9.05 % Adjusted Tier 1 leverage capital ratio, excluding PPP loans 10.63 % Bank: Tier 1 capital $ 147,262 Average assets for the leverage capital ratio $ 1,585,514 Less: Average PPP loans (424,290 ) Plus: Average PPPLF borrowings 188,222 Adjusted average assets for the leverage capital ratio $ 1,349,446 Tier 1 leverage capital ratio 9.29 % Adjusted Tier 1 leverage capital ratio, excluding PPP loans 10.91 % APPENDIX A

As of December 31, 2020Industry Concentration

We have a diversified loan portfolio, representing a wide variety of industries. Three of our largest categories of our loans are commercial real estate, commercial and industrial, and construction, land and land development loans. Together they represent $1.04 billion in outstanding loan balances, or 87.6% of total gross loans outstanding, excluding PPP loans of $365.8 million. When combined with $298.7 million in unused commitments the total of these three categories is $1.34 billion, or 88.9% of total outstanding loans and loan commitments.

Commercial real estate loans represent the largest segment of our loans, comprising 65.1% of our total balance of outstanding loans, excluding PPP loans, as of December 31, 2020. Unused commitments to extend credit represents an additional $20.5 million, the combined total exposure in commercial real estate loans represents $795.4 million, or 52.7% of our total outstanding loans and loan commitments, excluding PPP loans.

The following table summarizes our exposure by industry for our commercial real estate portfolio as of December 31, 2020:

(Dollars in thousands, unaudited) Outstanding Balance Available Loan Commitments Total Exposure % of Total

Loans

(Outstanding

Balance &

Available

Commitment)Average Loan Balance Number of Loans Hotel/Motel $ 120,018 $ 228 $ 120,246 8.0 % $ 4,445 27 Apartments 107,094 2,956 110,050 7.3 1,467 73 Office 79,712 3,008 82,720 5.5 876 91 Warehouse 78,732 1,900 80,632 5.3 1,575 50 Convenience Store 75,699 817 76,516 5.1 1,846 41 Retail 71,914 2,723 74,637 4.9 910 79 Mixed use 70,196 2,555 72,751 4.8 789 89 Mini Storage 38,923 528 39,451 2.6 2,780 14 Manufacturing 32,381 500 32,881 2.2 952 34 Groups < 2.0% of total 100,256 5,267 105,523 7.0 1,253 80 Total $ 774,925 $ 20,482 $ 795,407 52.7 % $ 1,341 578 Commercial and industrial loans comprise 14.6% of our total balance of outstanding loans, excluding PPP loans, as of December 31, 2020. Unused commitments to extend credit represents an additional $189.9 million, the combined total exposure in commercial and industrial loans represents $363.2 million, or 24.1% of our total outstanding loans and loan commitments, excluding PPP loans.

The following table summarizes our exposure by industry, excluding PPP loans, for our commercial and industrial loan portfolio as of December 31, 2020:

(Dollars in thousands, unaudited) Outstanding Balance Available Loan Commitments Total Exposure % of Total

Loans

(Outstanding

Balance &

Available

Commitment)Average Loan Balance Number of Loans Capital Call Lines $ 65,559 $ 128,208 $ 193,767 12.8 % $ 1,192 55 Construction/Contractor

Services14,089 26,046 40,135 2.7 99 143 Manufacturing 11,787 5,607 17,394 1.2 210 56 Family and Social Services 9,894 5,466 15,360 1.0 707 14 Medical / Dental /

Other Care12,300 2,376 14,676 1.0 192 64 Financial Institutions 13,400 - 13,400 0.9 3,350 4 Groups < 0.85% of total 46,329 22,181 68,510 4.5 150 309 Total $ 173,358 $ 189,884 $ 363,242 24.1 % $ 269 645 Construction, land and land development loans comprise 7.9% of our total balance of outstanding loans, excluding PPP loans, as of December 31, 2020. Unused commitments to extend credit represents an additional $88.4 million, the combined total exposure in construction, land and land development loans represents $182.8 million, or 12.1% of our total outstanding loans and loan commitments, excluding PPP loans.

The following table details our exposure for our construction, land and land development portfolio as of December 31, 2020:

(Dollars in thousands, unaudited) Outstanding Balance Available Loan Commitments Total Exposure % of Total

Loans

(Outstanding

Balance &

Available

Commitment)Average Loan Balance Number of Loans Commercial construction $ 43,511 $ 66,944 $ 110,455 7.3 % $ 1,813 24 Residential construction 21,632 16,245 37,877 2.5 1,082 20 Land development 10,405 4,505 14,910 1.0 946 11 Developed land loans 12,624 468 13,092 0.9 395 32 Undeveloped land loans 6,251 193 6,444 0.4 391 16 Total $ 94,423 $ 88,355 $ 182,778 12.1 % $ 917 103 Payment Modifications and Deferrals

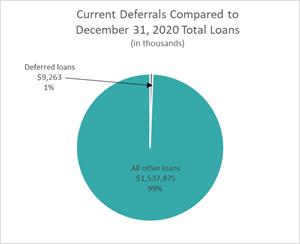

As part of our ongoing commitment to our customers we have been continuously proactive in contacting customers impacted by the stay-at-home order in Washington State, temporary business closures, or that have otherwise been impacted by the COVID-19 pandemic and responses thereto. As of December 31, 2020, $9.3 million in deferred or modified payments, pursuant to federal guidance, representing three loans, remained on deferred or modified status.

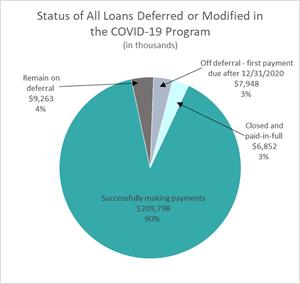

There was a total of $233.9 million, or 247 loans, granted deferred or modified payments in the quarters ended June 30, 2020 September 30, 2020 and December 31, 2020. As of December 31, 2020, $209.8 million, or 220 loans, have successfully resumed payments as scheduled, $7.9 million, or 7 loans, have moved to active status and have a payment due in the first quarter of 2021, $6.9 million, or 17 loans, have closed and paid-in-full, leaving $9.3 million, or 3 loans, on deferral.

The graph below illustrates the status of all the loans that were part of the COVID-19 deferral program:

View graph here: https://www.globenewswire.com/NewsRoom/AttachmentNg/eac49836-c27f-46a0-9a59-a54084ec55f1

The graph below indicates the percentage of loans that remain on a COVID-19 deferral. This illustration is based on total loans outstanding as of as of December 31, 2020.

View graph here: https://www.globenewswire.com/NewsRoom/AttachmentNg/c403935e-5443-44e0-ae4c-c3a529d56ff1

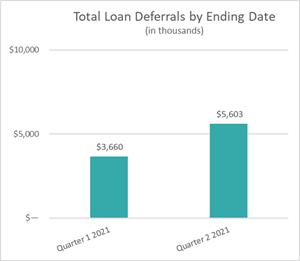

Remaining deferrals by deferral end date as of December 31, 2020:

View graph here: https://www.globenewswire.com/NewsRoom/AttachmentNg/78a0c167-4705-43a0-8739-58ce2faf0ed5

As a result of our proactive approach with customers, we did not see material downgrades in credit during quarter ended December 31, 2020 related to the COVID-19 pandemic. We will continue to be diligent in monitoring credit and changes in the economy, keeping the lines of communication open with our customers, but the full impact of these challenging economic times on our financial condition and liquidity remains to be seen at this time.

Status of All Loans Deferred or Modified in the COVID-19 Program

Status of All Loans Deferred or Modified in the COVID-19 Program

Current Deferrals Compared to December 31, 2020 Total Loans

Current Deferrals Compared to December 31, 2020 Total Loans

Total Loan Deferrals by Ending Date

Total Loan Deferrals by Ending Date